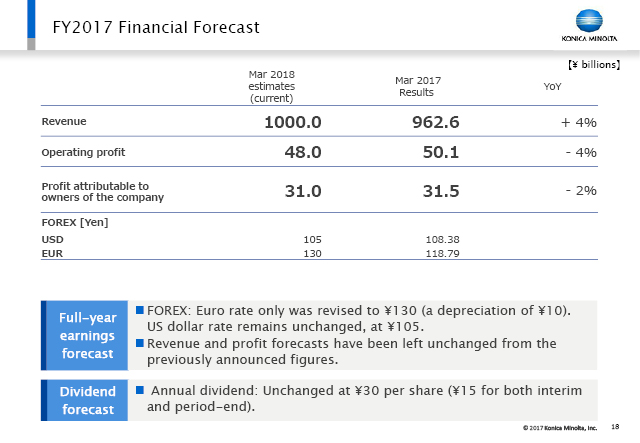

For the full-year earnings forecast, we are holding to the earnings forecast as of October 30.

Our assumption regarding exchange rates is to revise them in light of actual 3Q rates and the market rates. For 4Q, we only revised the euro rate downward by ¥10 (depreciating the yen) to ¥130. For the current fiscal year, we have engaged in management intended to achieve published forecasts without fail. While foreign exchange has had some impact, we are taking an extremely conservative approach and leaving our forecasts unchanged from previously announced figures. For dividends as well, the forecast remains unchanged at ¥30.

Our assumption regarding exchange rates is to revise them in light of actual 3Q rates and the market rates. For 4Q, we only revised the euro rate downward by ¥10 (depreciating the yen) to ¥130. For the current fiscal year, we have engaged in management intended to achieve published forecasts without fail. While foreign exchange has had some impact, we are taking an extremely conservative approach and leaving our forecasts unchanged from previously announced figures. For dividends as well, the forecast remains unchanged at ¥30.